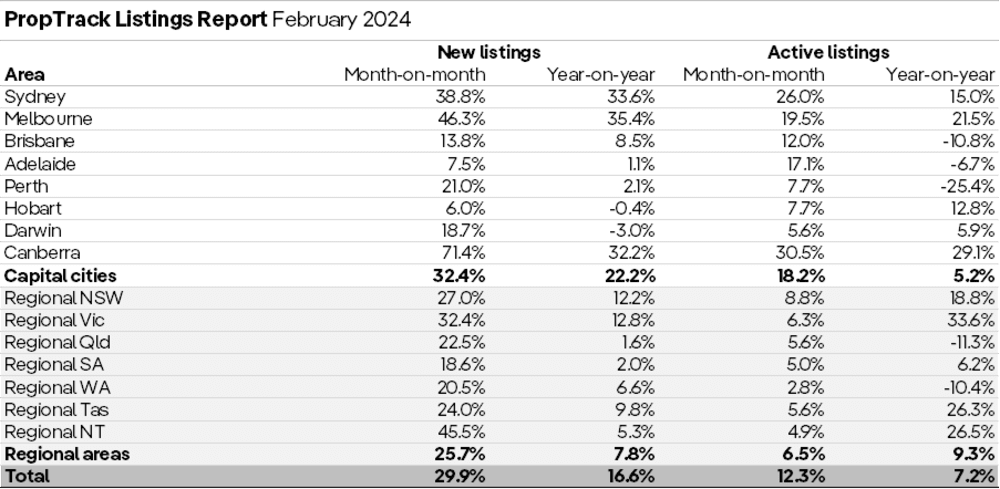

Australia’s property market accelerated in February, with a strong month of new listings coming to market. Nationally, there were 16.6% more new listings year-on-year.

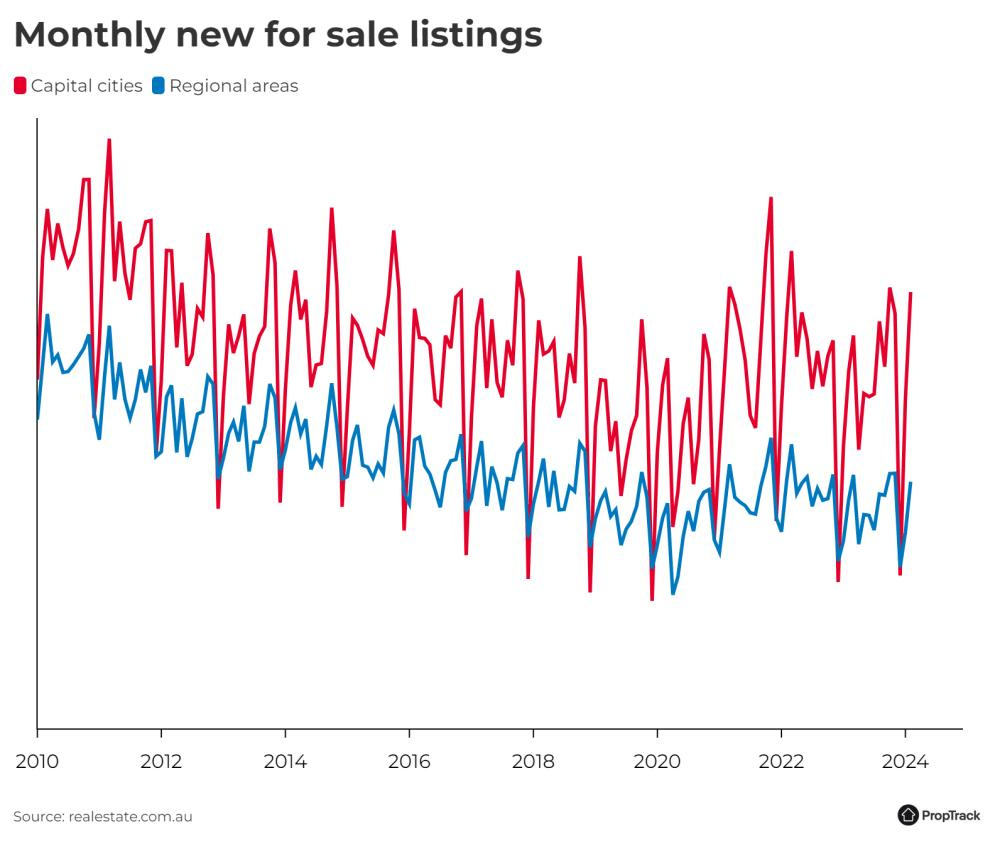

Capital cities led the busier activity, recording a stronger-than-typical February for new listings, and the most new listings across the combined capitals for a February since 2012.

The extra day in February due to the leap year will have raised volumes relative to non-leap years.

Regional areas were a little quieter, though not as quiet as 2023. Across the combined regional areas, February was broadly in line with the pace of activity that has been typical for February regionally over the past decade. Even so, the number of new listings regionally was up 7.8% year-on-year in February.

The total number of properties listed for sale across February was up 12.3% month-on-month nationally, with all markets across Australia recording increases.

In Sydney, Melbourne, Canberra, and Hobart the total number of properties listed for sale was sitting solidly above the prior-decade average; in Brisbane, Perth, and Adelaide, it was sitting around 40% below.

Outlook

Property markets in capital cities, Sydney and Melbourne especially, saw a strong start to 2024, with the busiest January and February since 2012 across the combined capital cities. This followed a period in 2023 of more-normal spring activity than was the case in 2022, when activity was fairly quiet.

Supporting this busier start to the year – more so than we were seeing in spring 2022 and early 2023 – was strong demand, unemployment that remained low by historical standards, strong population growth, tight rental market conditions, and a more stable outlook for interest rates.

Markets are no longer expecting a further increase in interest rates, with an expectation of cuts as soon as the second half of this year. This is driven by the fact inflation appears to be coming under control sooner than the RBA had initially anticipated: over 2023, inflation was 4.1% compared to the RBA’s expectation of 4.5%. The RBA is now expecting inflation will be close to their target by the end of this year.

Regional NSW and regional Victoria saw solid increases in new listings compared to the same time last year, continuing their trend of improving activity and choice since the end of 2021. In fact, the total number of listings in regional Victoria has almost returned to its average over the past decade and is higher than it was pre-pandemic – a sharp turnaround from where it stood in the middle of 2021, when it was down more than 60% compared to the decade average.

Source: REA Group

Cover Image Source: Canva (Zstockphotos)